It’s been a couple of weeks since the federal budget announcement and since then we’ve had some time to review how the proposed changes relating to plant and equipment deductions will affect property investors.

It’s been a couple of weeks since the federal budget announcement and since then we’ve had some time to review how the proposed changes relating to plant and equipment deductions will affect property investors.

Although we are not expecting the legislation to be finalised anytime soon, we have been talking with government with the aim of developing fair policy which covers all the necessary factors.

Many investors who have contacted us have asked how they will be affected. The proposed changes won’t have any effect on properties that are already owned. It will only affect owners who have exchanged contracts on an investment property after the 9th of May 2017.

Below are the key points to answer the questions investors have relating to the proposed changes. Because the legislation is yet to be finalised, it is important to note that further changes may still take place.

What changes have been proposed?

- Subsequent owners (those who purchase a second hand property) who exchange contracts after the 9th of May 2017 will not be able to claim depreciation on existing plant and equipment assets

- Although there is nothing specific mentioned about new properties, we expect that investors will be able to depreciate new plant and equipment assets within a new property as they have been previously. This will continue as normal

- Any additional assets added to a property can be depreciated as normal.

- Investors will still be eligible to claim qualifying capital works deductions, which are the deductions available on the structure of the building. This includes any additional capital works carried out by themselves or a previous owner. The Capital works deduction is available on properties that commenced construction after the 16th of September 1987

- The budget notes advise that existing investments will be grandfathered. This means that any investor who exchanged contracts prior to the 9th of May 2017 can still claim plant and equipment depreciation per normal

What is plant and equipment?

- These are the easily removable or mechanical assets found within an investment property

- Some examples include air conditioners, hot water systems, smoke alarms, garbage bins, blinds and curtains

- The Australian Taxation Office provides individual effective lives for plant and equipment which can be used to calculate the rate of depreciation over time

When will the changes take place?

- The proposed new legislation will be in force from the 1st of July 2017

Who will be affected by this change?

- Property investors who exchanged contracts to purchase a second hand residential property after 7:30pm on the 9th of May although the new rules won’t be applicable until after July 1 2017

How will these investors be affected?

- These investors will only be able to claim plant and equipment depreciation on the assets they purchase and add to the property themselves

- Investors who purchase a second hand property should still contact a specialist Quantity Surveyor to discuss the deductions they can claim for qualifying capital works deductions

Who won’t be affected by these proposed changes?

- Owners of brand new residential properties who exchanged contracts both before and after the 9th of May

- Residential property investors who exchanged contracts prior to the 9th of May 2017

- Commercial property owners and their tenants can continue to use the existing rules. It is our understanding that the changes relate only to residential investment properties

- Home owners are unaffected as only income producing properties will be impacted. However, those who decide to turn their primary place of residence into an investment property are only affected if their property was purchased after the 9th of May 2017. If a home owner purchased their property prior to the 9th of May 2017 and they decide later to rent it out, owners can use the pre-existing depreciation legislation

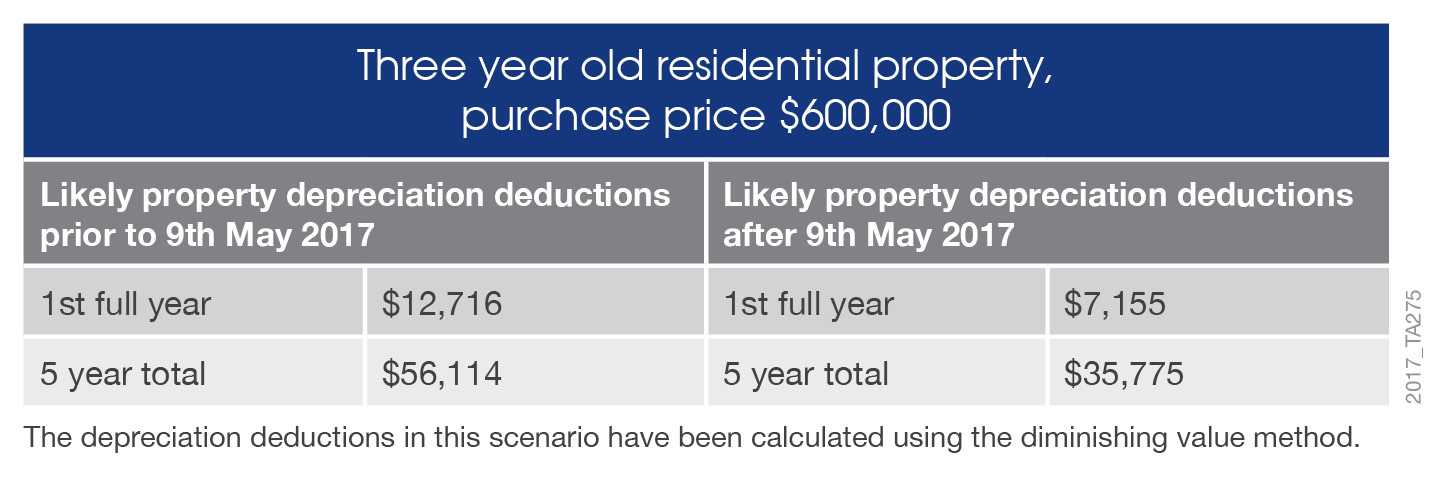

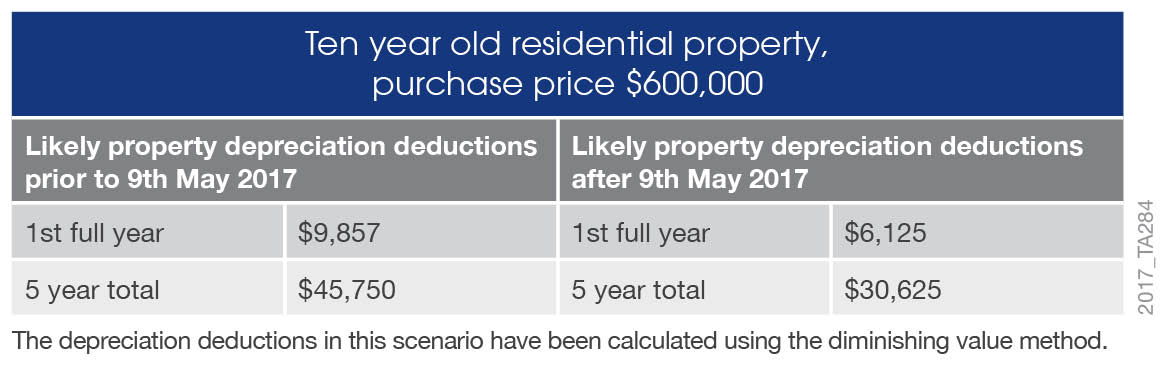

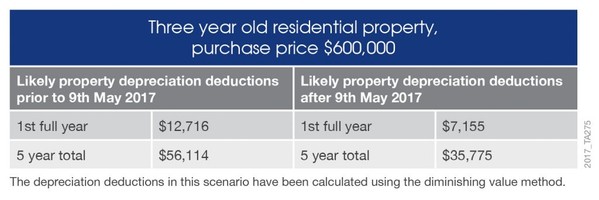

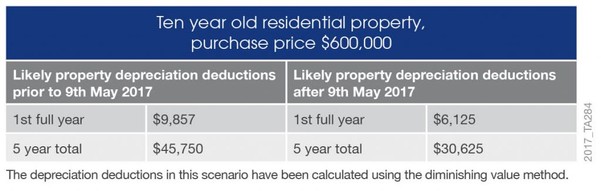

Depreciation scenario – before and after 9th of May

The following tables show the deductions an investor would receive for both a three year old and a ten year old residential property purchased for $600,000. They examine the deductions an investor who exchanged contracts prior to the 9th of May could claim compared with the likely depreciation deductions they could claim if they exchanged contracts after the 9th of May under the proposed new legislation.

This information has been kindly supplied by BMT Quantity Surveyors, to request more information please click here